Bitcoin's paradigm shift and ETF prospects

Bitcoin's paradigm shift and ETF prospects

The Bitcoin Newsletter 16

Welcome to the 16th edition of The Bitcoin Newsletter

As it will be the last edition of 2023 I would like to thank you sincerely for your interest in my thoughts and the engagement I have received from you. This newsletter started with the intention to funnel my thoughts and share these with anyone who might be interested. Beyond that in the past 12 months it became a great motivator to dig deeper and build a stronger community of Bitcoiners around me. This outcome was not intended and I’m very grateful for the journey so far - Thanks to you!

To wrap up this year, I'm going to discuss a phenomenal talk from Parker Lewis from a few weeks ago where he discussed how Bitcoin is much more than just an inflation hedge, it's a paradigm shift. Specifically, I will delve into this topic and discuss what that exactly means. Furthermore, I will also give a brief projection for 2024, which looks promising with the upcoming halving in April and a number of potential Bitcoin ETFs approvals.

We wish you and your family a Happy New Year and look forward to discussing a range of exciting topics with you in the coming year. Thank you for your engagement!

Best Regards,

Leon

DEEP DIVE

Bitcoin ETFs on the Horizon: Decoding Paradigm Shifts and Learning from Gold's Trajectory

At Dallas' world-class business campus, Old Parkland, Parker Lewis explained why Bitcoin is the ultimate solution to monetary inflation, how Bitcoin adoption occurs over time, and why Bitcoin is the greatest asymmetric opportunity today. I highly recommend you to watch the talk VIDEO.

That sounds promising, but what exactly does that mean? For me, Bitcoin means the mental exit from the fiat system. It is not about compensating for inflation, but about being part of a system in which there is no inflation in the long term.

Bitcoin is disinflationary, meaning supply decreases over time until the last fraction of a Bitcoin is mined in 2140. After that there will be no more inflation.

Currently, Bitcoin's annual inflation rate stands at approximately 1.8% and will decrease to 0.9% after the upcoming halving, scheduled for Friday, April 19, 2024 at 01:53:42 AM UTC. The inflation rate is then already negligible. The halving reduces the block reward by 50%, i.e. the Bitcoin given to miners every 10 minutes for the successful verification of transactions.

On average, the halving occurs every four years, or after every 210,000 transaction blocks mined, until all 21,000,000 Bitcoin have been mined (in the year 2140). The next halving is expected to reduce the block reward from 6.25 Bitcoin to 3,125, which is equivalent to 900 to 450 Bitcoin to be mined daily.

For most it is hard to imagine what this means for the price of an asset. Before Bitcoin, humanity did not know an absolute scarce good. Even gold has an elastic supply. When demand increases, more effort can be put into mining gold, but this is not possible with Bitcoin.

This essentially means that the price rises with every halving (i.e. a reduction in supply). This in turn creates buzz and more demand. This is how the exponential Bitcoin bull markets arise. To me it no longer makes any sense at all to own another asset to store value. No asset can compete with Bitcoin. Bitcoin is therefore not an inflation hedge, but rather a paradigm shift.

It has become the basis of my work and my life. When making economic decisions, I no longer base them on interest rates from central banks or government decrees, but rather on the supply plan of Bitcoin.

This pure price signal that cannot be manipulated by any central actor (which is one of Bitcoin's central innovations) sets the "tone" for my economic existence.

As Bitcoin makes its way into traditional financial markets, it is expected that the Bitcoin issuance plan will become increasingly important to financial markets and the central bank's decision will become less and less important.

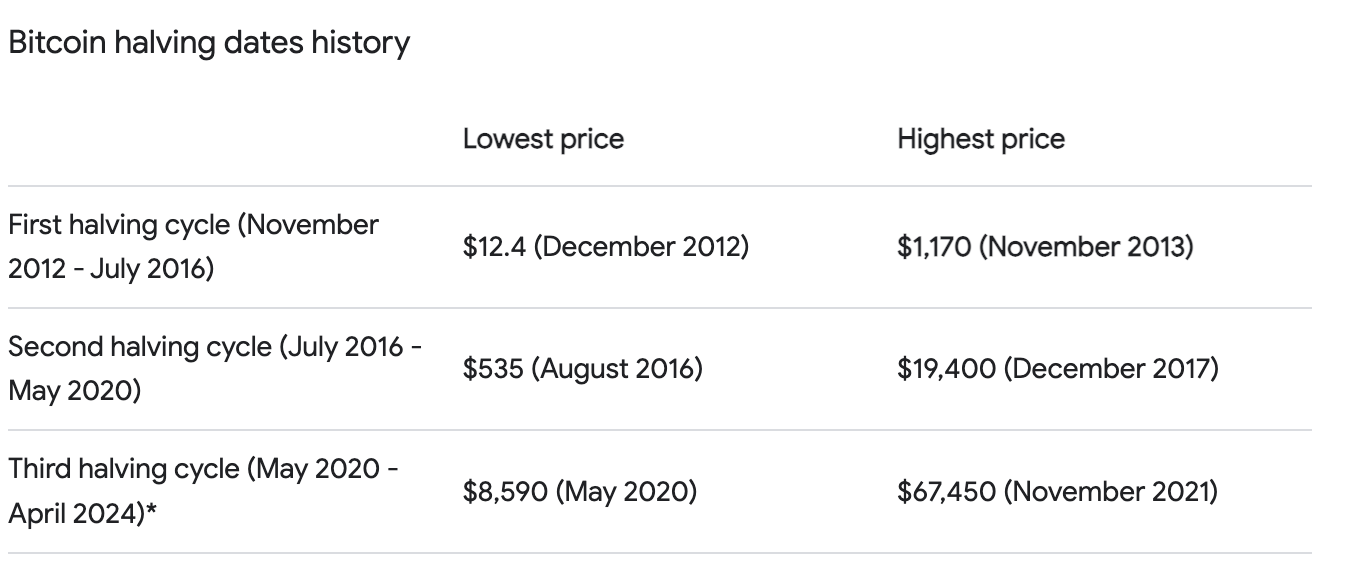

Since Bitcoins inception in 2009 three Bitcoin halvings have taken place. The first Bitcoin halving took place in November 2012, the second in July 2016, the third in May 2020, and the fourth is about to take place on April 19th 2024.

Historically, the Bitcoin price has increased exponentially around every halving with a bull market the following year. As you can see in the “Bitcoin halving dates history” chart below, after each halving, the Bitcoin price has increased from bottom to top by 9335.5% (2012 - 2013), 3526.1% (2016 - 2017), and 686.3% (2020 – 2021) respectively.

*Third halving cycle is not yet completed, so the low and high are determined with price data as of December 30, 2023. Fourth halving date is estimated.

Source: Bitcoin Halving Dates: When Is the Next BTC Halving?

These exponential price increases are related to the multiplier effect. A scarce commodity like Bitcoin does not require large capital inflows to increase in price because supply is extremely limited.

Imagine an asset with a supply of 10. The last selling price was $30,000. This means a market cap of the asset is $300,000 (10x30,000). The most recent sales price is multiplied by the existing units to determine the market capitalization of an asset.

If 9 units of that good are in the hands of several people who do not want to sell, and only 1 unit is available on the market, demand for that one unit is likely to be high. The seller can therefore decide for what price she wants to sell the asset. If the seller decides to sell the asset for $50,000 the market capitalization is $500,000 (10x50,000). Although only $50,000 of new liquidity has entered the market, the market cap has increased by $200,000. This is the multiplier effect.

The multiplier effect affects an extremely scarce commodity like Bitcoin, which is held in the hands of people who do not want to sell. Once you grasp how Bitcoin operates, selling becomes practically irrelevant.

Bitcoin long-term HODLER supply is at an all-time high. Around 76% of the circulating supply of Bitcoin has been held untouched for over one year. This extremely tight supply will meet unprecedented demand.

On the one hand, macro and geopolitical issues have caused stock markets worldwide to weaken, which will result in many people turning to Bitcoin to generate alpha.

On the other hand, Bitcoin is finding its way into traditional finance. Wall Street is undergoing a significant transformation as it increasingly embraces Bitcoin.

Currently, several of the world’s largest asset management firms have submitted spot Bitcoin ETF applications for review by the SEC.

These financial heavyweights such as BlackRock, Fidelity, Invesco, Franklin Templeton Investments, Wisdom Tree, VanEck, Global X, Ark Invest, Valkyrie, Bitwise Asset Management, and Galaxy Digital have approximately $16.7 trillion in total assets under management (AUM). Only a fraction of their AUM invested into spot Bitcoin ETFs can have a massive impact on the price of Bitcoin.

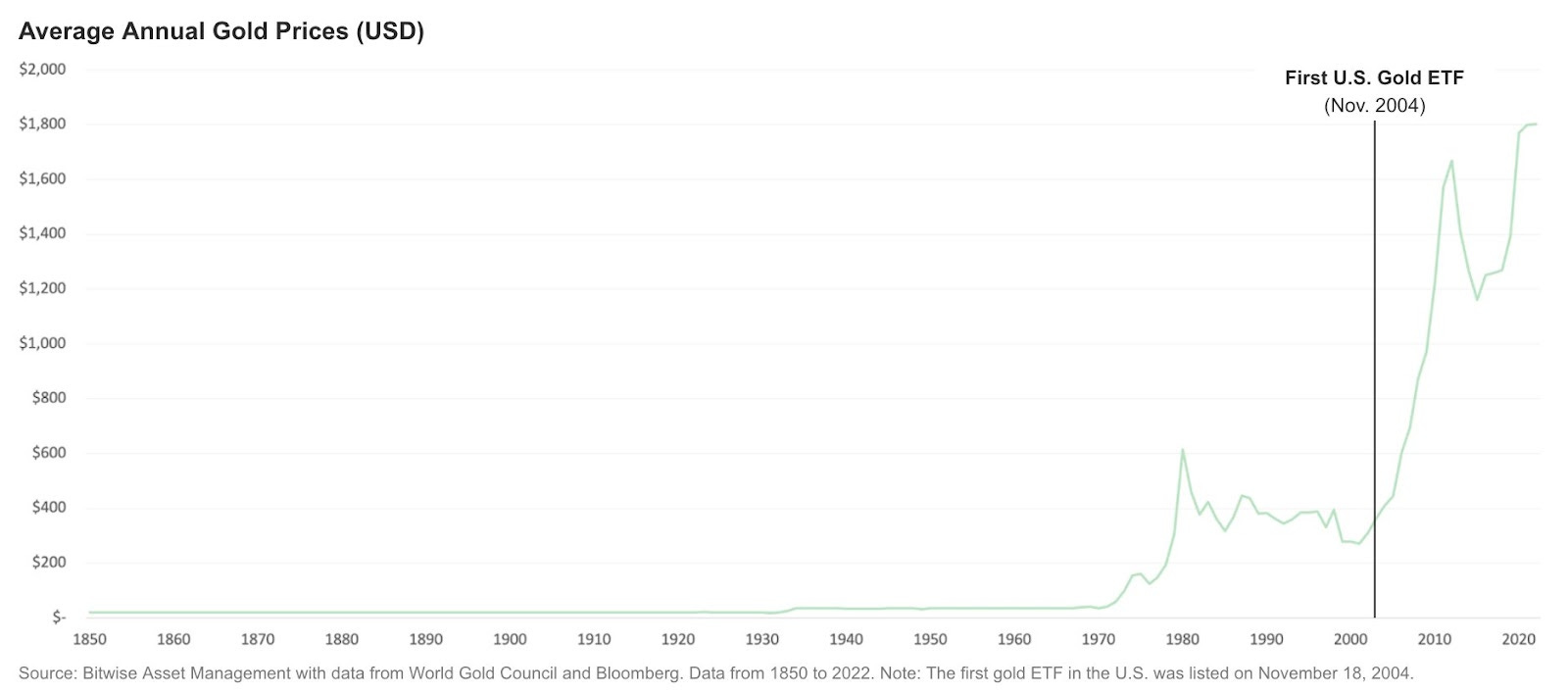

In parallel with Bitcoin's integration into traditional finance, the imminent approval of Bitcoin ETFs draws inspiration from the transformative journey of gold ETFs.

Galaxy Digital's report, Sizing the Market for a Bitcoin ETF, envisions significant inflows into Bitcoin, projecting a potential 74% surge in Bitcoin's price within the initial year of the release of a Bitcoin ETF, echoing the impactful evolution seen with gold ETFs. Examining Bitcoin's smaller market cap and supply in investment vehicles, the analysis hints at an 8.8x greater potential impact compared to gold.

This comparison underlines Bitcoin's paradigm-shifting potential, providing investors with valuable perspectives as the ETF landscape unfolds.

Note: The first gold ETF in the U.S. was listed on 18. November 2004.

Source: Bitwise Asset Management, Sizing the Market for a Bitcoin ETF report with data from World Gold Council and Bloomberg. Data from 1850 to 2022.

I expect a phenomenal bull market. However, regardless of my expectations, I don't want to make a price diagnosis; It is almost impossible to predict the future or the Bitcoin price. But what I would like to emphasise is that I assume that we will exceed the $100K price per Bitcoin faster than we can imagine.

I would like to point out that I also expect a crash. As always, investors will take it upon themselves to borrow money at inopportune times to buy Bitcoin, which can lead to a margin call if the price is weak. This usually creates a sales cascade that takes on its own momentum and pushes the price downwards. Until a bottom is found and the game of price discovery begins again.

This is a feature of the Bitcoin network, not a bug. Because it clears the market, leads to real price signals and antifragility over time, as investors and businesses have to adapt to these price dynamics and develop robust investment strategies and business practices.

In broader context, Bitcoin's success is not about reaching a new all-time high (ATH) for the Bitcoin price, but rather about securing a higher low compared to the previous bear and bull cycles.

I'm uncertain about the precise trajectory these dynamics will take, but I eagerly anticipate navigating this journey with all of you. Following the challenges of this bear market, our excitement is palpable as we anticipate the forthcoming bull market.

WORTH TO KNOW

Podcast and publications

Bitcoin Magazine: Bitcoin is Kosher

In my latest article for Bitcoin Magazine I explain why Bitcoin is kosher and forms the basis for a financial system compatible with Jewish ethics. READ

Real Estate investors are flocking to Bitcoin in record numbers

Switzerland-based Bitcoin exchange Relai has disclosed to Bitcoin Magazine that a staggering 75% of its Over-The-Counter (OTC) revenue in the final quarter of 2023 stemmed from private clients diverting proceeds from real estate sales into Bitcoin, showcasing a seismic shift in investment strategies among investors. I've long predicted that real estate investors would diversify into Bitcoin, now it’s starting to happen. In an article by Bitcoin Magazine on the topic, the Relai CEO Julian Linger and I have been quoted. READ

The future of Bitcoin & Real Estate

A few months ago I was a guest at the Hotel Princess Plochingen, the first Bitcoin hotel in the world, to talk about the advantages of Bitcoin over real estate and the future of the two asset classes as part of the “Bitcoin Block” educational initiative. The German interview is now online. WATCH

IDEAS OF INTEREST

The Fundamentals of Bitcoin’s Price - One of the unique things about Bitcoin is that supply and demand can actually be determined and measured. In this article, Arman The Parman explains what information this gives us about Bitcoin's price.

If you want to support me. Feel free. You can send me some satoshi/bitcoin.

My lightning address is: law@getalby.com

My bitcoin address is: bc1qyc9q89wjzmvaw729tj3wsrsfhft53mjycrjxdk

Nostr PubKey

npub1v5k43t905yz6lpr4crlgq2d99e7ahsehk27eex9mz7s3rhzvmesqum8rd9

Resources

Bitcoin is not a hedge | Parker Lewis at Old Parkland

Hodling hard: Bitcoin’s long-term investors own over 76% of all BTC for the first time

Galaxy Digital - Sizing the Market for a Bitcoin ETF

Photo Credit: Wall Street by Paul Strand, 1915.

{kind=link}

Disclaimer: the content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Make sure you do your own research before making any investment and be aware of your own risk tolerance. If you like to build on my thoughts, feel free, but please cite me as the source. 2023 - Leon A. Wankum.

Editing and content creation by Clemens Haidinger.

And the synthetic Bitcoin on every other chain?

WBTC, BTCB etc.

These are exactly the same price as bitcoin and can be swapped for native bitcoin 1:1

With Defi, we create loans which is to create new bitcoin - we are the bank operating fractional reserve banking.

My point is there must be more BTC on the other chains than the native chain.

And in time we shall see the whole circulation as M2, with native Bitcoin M1 money supply.

But in conclusion there will be a lot more than 21 milliion units.

Defi has its own minting & inflationary process.

So how does this fit in with the deflationary bitcoin concept?

As long as we have collateral, we can create new bitcoin.